Founder: Nicolas Burtey

Date Based: September 2019

Location of Headquarters: United States

Variety of Workers: 11

Web site: https://www.galoy.io/

Public or Non-public? Non-public

Final week, Galoy launched Lana, software program that permits banks to simply accept bitcoin as collateral for loans.

Lana helps group and challenger banks (the banks with which Galoy is seeking to work) to supply bitcoin-backed loans to numerous varieties of prospects.

“Some banks would possibly need to use it to promote to retail, and a few would possibly need to use it to promote industrial prospects or high-net-worth people,” Burtey informed Bitcoin Journal.

In providing such loans to a wide selection of shoppers, Burtey believes that the excessive price of borrowing presently related to such merchandise will come down.

“As we speak’s rates of interest are 12% to fifteen% if you wish to get a mortgage utilizing your bitcoin as collateral,” stated Burtey.

“The charges are excessive as a result of there are so few monetary establishments providing such a product. We see a possibility now that the laws are permitting banks to do issues with bitcoin,” he added.

“We expect loads of banks will need to enter this market.”

If Burtey is right in his prediction that banks are eager to supply bitcoin-backed loans, this won’t solely decrease charges for such loans, however it is going to additionally introduce open-source Bitcoin software program into the world of banking, which might provoke a brand new development within the business.

However extra on that in only a minute. First, some background on Galoy.

Galoy’s Historical past: From Blink Pockets To Lana

Based in September 2019, Galoy had intentions to allow banks to make use of bitcoin from the beginning, but it surely needed to maintain off on doing so attributable to an unfriendly regulatory setting.

So, as a substitute, it centered its efforts on creating and supporting Blink wallet (which was initially referred to as the Bitcoin Seaside pockets and which Galoy just lately offered), a custodial Bitcoin and Lightning pockets predominantly used at first in El Salvador after which in Bitcoin circular economies globally.

“Galoy’s mission was to onboard banks to Bitcoin 5 years in the past,” stated Burtey.

“However the regulatory setting was so dangerous over the past 5 years that we determined to create Blink. The explanation we are actually specializing in our unique mission is as a result of with the tip of Choke Point 2.0 and the repeal of SAB 121, we predict now could be the right time to assist banks undertake Bitcoin.”

Burtey spoke about his work in creating and rising Blink fondly and shared that he needed to cease engaged on the undertaking solely as a result of it could be too tough to proceed managing it whereas additionally aiming to serve a brand new kind of clientele.

“Blink is a B2C (Enterprise-To-Buyer) play, and it’s arduous as an early-stage startup to give attention to too many issues,” defined Burtey.

“Galoy is a B2B (Enterprise-To-Enterprise)-driven enterprise, and we need to work with banks and monetary establishments,” he added.

“It’s good to be centered on only one factor.”

And, as talked about, that one factor will now be Lana.

How Lana Works

Lana is software program that Galoy helps banks combine and handle for a subscription price. With this software program, banks can challenge bitcoin-backed loans underneath the phrases they create.

“We’re not those deciding how a lot curiosity will likely be charged or something like that,” defined Burtey.

“We give banks the platform to do that, after which they will work out their price of capital, the length of the mortgage, the liquidation value for the bitcoin within the mortgage and the speed at which they need to lend,” he added.

“We’re supplying you with software program, and serving to you run and automate that software program.”

One thing else that Galoy doesn’t do for banks is custody the bitcoin offered as collateral for the loans they challenge. Every of the banks with whom the corporate works is accountable for choosing their very own custodian.

“You possibly can go to BitGo or Fireblocks or every mortgage can have its personal multisig,” stated Burtey. “We’re agnostic on custody.”

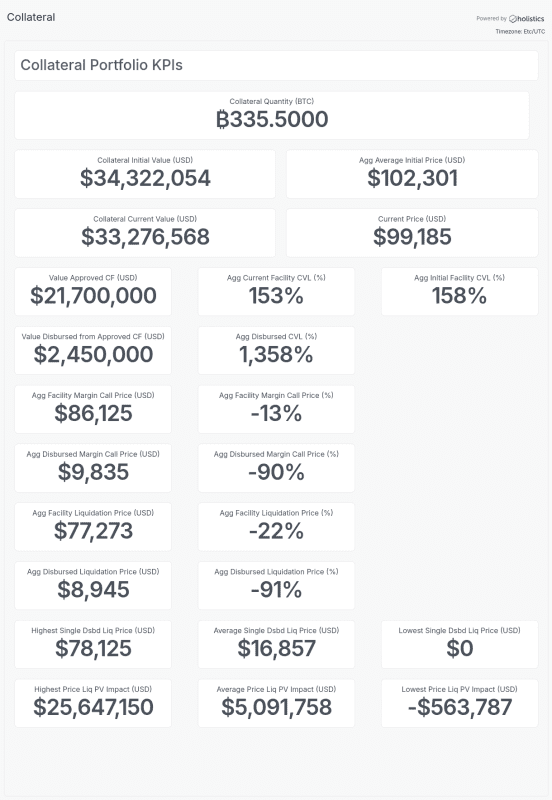

With that stated, Lana helps banks monitor the bitcoin in custody in order that banks can pay attention to whether or not or not collateral is nearing liquidation ranges.

“A key piece of this product is threat administration,” stated Burtey.

“Bitcoin is risky, and the financial institution will want a software to indicate that it’s taking calculated threat. So, we’ll present banks with a dashboard to observe this threat,” he added.

Who Will Use Lana?

Galoy is focusing on group banks and different smaller monetary establishments with this new product largely as a result of they suppose these smaller gamers will profit most from it — and since the large banks possible gained’t want such a product.

“We do not suppose JP Morgan will actually need to work with us,” stated Burtey. “They’re in all probability constructing one thing like this themselves, whereas a smaller financial institution, a credit score union or small firm in all probability isn’t.”

Burtey additionally understands that smaller lenders’ incorporating Lana versus constructing one thing comparable themselves can save these monetary establishments a big quantity of effort and time.

“Our purpose is to say, ‘Look, you’ll be able to develop this internally, and it’ll take you six months, a 12 months or longer relying on how a lot you already know about Bitcoin,’” stated Burtey. “‘Or now we have a lending product as a service for you, and you’ll launch it far more shortly.’”

And as Burtey and his staff onboard their first spherical of smaller banks, they’ll not solely be making historical past in enabling extra banks to simply accept bitcoin as collateral for loans, however they’ll probably be altering the trajectory of banking normally by introducing open-source software program to it.

Open-Supply Bitcoin Banking

Burtey’s long-term imaginative and prescient for Galoy is to do far more than simply assist banks challenge bitcoin-backed loans. He’s seeking to introduce open-source software program into banking as extra banks start to embrace Bitcoin.

Nonetheless, it’s necessary to notice that Lana isn’t open-source simply but. It’s fair-source software program, and, underneath such a license, code turns into open-source after two years.

“It is a delayed open-source system, but it surely’s all obtainable on GitHub,” stated Burtey. “You possibly can go and check out it, take a look at it, and play with it by yourself.

Underneath the fair-source license, no firm aside from Galoy can promote the product to a financial institution proper now, permitting Galoy to revenue whereas nonetheless constructing with auditable code.

“We promote the deployment, and we assist banks to plug in to their custodian,” defined Burtey. “We’re constructing within the open — however we additionally need to generate income.”

Past serving to banks implement Lana, Burtey’s needs to develop open-source “core banking software program,” as he’s seeking to disrupt the “core ledger” oligopoly.

“The core ledger is the place banks retailer the account knowledge, buyer info and transaction particulars,” stated Burtey. “It’s the supply of fact for banks.”

And solely three firms — FIS, Fiserv and Jack Henry — have the core ledger market cornered.

“These are all like hundred billion greenback firms that you just’ve in all probability by no means heard about as a result of all they do is give attention to promoting software program to banks,” stated Burtey.

“Our long-term purpose is to disrupt this business by making one thing that’s open supply,” stated Burtey. “As we speak, there isn’t any firm that does core banking with the thought of open supply, and so we’re working in direction of this.”

Burtey envisions a world through which open-source software program could make it a lot simpler for somebody to start out a Bitcoin financial institution. (For individuals who wince on the phrases “Bitcoin” and “financial institution” being utilized in tandem, would possibly I remind you that it was the legendary Hal Finney himself who wrote that bitcoin-backed banks would function a scaling resolution.)

“To start out a financial institution right this moment is a really costly and complex course of,” stated Burtey. “It’s important to pay $100,000 plus simply to buy the core ledger expertise.”

Burtey then referenced his personal expertise in beginning Blink pockets, primarily a bitcoin financial institution run on open-source code, earlier than persevering with.

“I simply went to El Salvador and began what was successfully my very own financial institution as a result of I needed to,” stated Burtey.

“We have to reinvent how core banking software program is being made on this planet of Bitcoin, and I believe that is the place open-source turns into related,” he added.

“That is actually why I believe the world of banking and Bitcoin will likely be very totally different from the world of banking with fiat, and I believe we’re one of many firms on the forefront of this.”